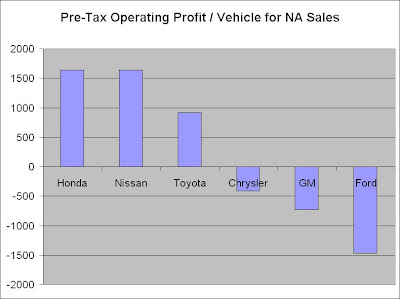

ould be forced to declare bankruptcy before they would be able to receive any federal aid. Thus, they came to the government asking for more money with fewer strings attached. Under the current program, the money, coming in the form of loans, would only be used to help the companies develop more fuel efficient cars. Leaders in the federal government are torn. Generally, Republicans believe that the problems American car manufacturers are experiencing are a result of their financial mismanagement and faulty business plan (see below, left). They do not believe we should bail them out, for it would be another instance of taxpayers paying for poor management of companies. Democrats claim that failure in the domestic auto manufacturing industry would be detrimental to the health of our economy and would cost Americans up to 3 million jobs. Because of how divided our government is on the issue and despite the fact that I have come to my own conclusions about the $700 billion Troubled Assets Relief Program (TARP), I decided to explore the blogosphere to get a feel for what the public and experts believe about this bailout and to leave my feedback on them. The result was overwhelming. I expected to find equal parts positive and negative feedback on the issue, but I found it hard to find any supporting commentary by economists or financial experts. Of those sites, I found two that were especially interesting. The first, “Demand More for Your Auto Bailout Dollar; Oil Patch Should Bounce Back Long Term” by Michael Fitzsimmons of Seeking Alpha, Fitzsimmons discusses what conditions the government should put on any money they give to the auto industry in order to maximize its benefit to the country as a whole. Peter Cohan, of BloggingStocks, writes about how taxpayer dollars can be best utilized to help the auto industry, and GM in particular, in a post entitled “Six Steps to Restructure GM”. Overall, I agree that the current bailout is not justified. There need to be more restrictions and covenants on the money that is being given to the auto industry. Whether that is to make the companies greener or to save taxpayers more money, it does not matter. In addition to posting my comments on the blogs, I have copied them below.

ould be forced to declare bankruptcy before they would be able to receive any federal aid. Thus, they came to the government asking for more money with fewer strings attached. Under the current program, the money, coming in the form of loans, would only be used to help the companies develop more fuel efficient cars. Leaders in the federal government are torn. Generally, Republicans believe that the problems American car manufacturers are experiencing are a result of their financial mismanagement and faulty business plan (see below, left). They do not believe we should bail them out, for it would be another instance of taxpayers paying for poor management of companies. Democrats claim that failure in the domestic auto manufacturing industry would be detrimental to the health of our economy and would cost Americans up to 3 million jobs. Because of how divided our government is on the issue and despite the fact that I have come to my own conclusions about the $700 billion Troubled Assets Relief Program (TARP), I decided to explore the blogosphere to get a feel for what the public and experts believe about this bailout and to leave my feedback on them. The result was overwhelming. I expected to find equal parts positive and negative feedback on the issue, but I found it hard to find any supporting commentary by economists or financial experts. Of those sites, I found two that were especially interesting. The first, “Demand More for Your Auto Bailout Dollar; Oil Patch Should Bounce Back Long Term” by Michael Fitzsimmons of Seeking Alpha, Fitzsimmons discusses what conditions the government should put on any money they give to the auto industry in order to maximize its benefit to the country as a whole. Peter Cohan, of BloggingStocks, writes about how taxpayer dollars can be best utilized to help the auto industry, and GM in particular, in a post entitled “Six Steps to Restructure GM”. Overall, I agree that the current bailout is not justified. There need to be more restrictions and covenants on the money that is being given to the auto industry. Whether that is to make the companies greener or to save taxpayers more money, it does not matter. In addition to posting my comments on the blogs, I have copied them below.“Demand More for Your Auto Bailout Dollar; Oil Patch Should Bounce Back Long Term”

Comment:

Thank you for your thoughtful and insightful commentary on the proposed bailout of the A

merican automobile industry. I liked how you approached the issue not as a simple yes or no to the bailout, but more of constructive commentary as to how the terms of any loans to the automobile companies can be amended to create a sustainable industry dynamic and to best benefit the country as a whole. I agree that U.S. automakers are to blame for much of the problems our economy is experiencing by producing sub-par products that increased our dependence on foreign oil and pushed consumers to foreign products. In the end, I do not believe the question is if the automobile industry will receive more money from the government. Based on its track record, the question is more when and under what terms.

merican automobile industry. I liked how you approached the issue not as a simple yes or no to the bailout, but more of constructive commentary as to how the terms of any loans to the automobile companies can be amended to create a sustainable industry dynamic and to best benefit the country as a whole. I agree that U.S. automakers are to blame for much of the problems our economy is experiencing by producing sub-par products that increased our dependence on foreign oil and pushed consumers to foreign products. In the end, I do not believe the question is if the automobile industry will receive more money from the government. Based on its track record, the question is more when and under what terms.I agree with your ideas that they must make a natural gas powered car and that they should strive to make cars that get over 40 MPG. That is the most sustainable approach and it also benefits every person in the country by reducing our emissions However, I do not agree that every vehicle must get over 40 MPG or that “every vehicle they make must be natural gas, hybrid, or electric”. Engines and batteries have not reached the level of technology that they are capable of being reliably installed in every vehicle. Did you forget about commercial vehicles that must be used to tow heavy loads? How can you expect vehicles like that to use a less powerful hybrid or electric engine or to achieve such a high gas mileage? Additionally, until there are better ways of getting natural gas to every consumer, it does not make sense for a large percentage of vehicles to be powered exclusively by natural gas.

Once again, thank you for taking a different approach to this issue than many other people do. It is so easy to say no without giving any sort of alternative. Hopefully, the federal government will pay attention to people like you and realize that there are better ways to approach this problem and use this money to actually improve our automobile industry rather than temporarily slow its failure.

“Six Steps to Restructure GM”

Comment:

Thank you for an interesting piece on your approach to the problems the U.S. automobile industry. I liked the fact that you took a stance that so many people have overlooked or deemed impossible, despite the fact that it is one that makes the most sense. Bankruptcy was created for companies in GM’s exact situation and it does not make sense that people cannot see that. Admittedly, we are living in a time of potentially extenuating circumstances, for the economy is in such bad shape and the stock markets so volatile that news of GM declaring for Chapter 11 protection might trigger a chain reaction that would end up destroying our economy.

The government eventually will have to put some money into the automobile industry, but not in the way it is currently planning. I think your ideas make the most sense. If people really do want to see change in companies like General Motors, then force it to declare bankruptcy and then provide the financing to restructure once it has done so. Your talking points, of merging with Chrysler, getting rid of unprofitable brands, closing related dealerships, merging Chrysler and GM brands, and cutting pay all make sense and should have been done if not for one problem that you also provide a remedy for. The management must be replaced. Your fact that GM’s CEO has “presided over a 95% decline in the company stock over his tenure” is shocking, and I agree that we cannot expect any changes if the person who started this decline remains in a position of authority.

One thing I would have liked to have seen is more talk about how to address the issue of renewable energy and increased vehicle efficiency. I agree that it may not make sense to set an immediate requirement for achieving a certain level of emissions, but does it not make sense to set some sort of timetable for requiring them to get on the right track in terms of research and development and future models?

{kind=link}